Why Are These Markets So Expensive?

The underlying causes differ by geography, population size, and economic stability, but they share a common theme: high cost structures combined with limited alternatives.

1. Geographic and Population Constraints

Small island territories and microstates face disproportionately high infrastructure costs. Subsea cables, landing stations, backbone equipment, and maintenance must be funded by a tiny subscriber base. In places like Saint Helena or São Tomé, this naturally raises the cost per user.

2. Economic Pressures and Currency Volatility

In countries such as Zimbabwe, extreme fluctuations in foreign exchange markets, unstable inflation, and currency shortages force mobile operators to anchor prices to more stable currencies (usually USD). This results in steep nominal data prices.

3. Power and Operational Expenses

Unreliable electricity grids mean towers often run on diesel generators or large battery banks, significantly raising ongoing operating costs. In remote or rural regions, simply powering a network site becomes a costly challenge.

|4. Limited Market Competition

High taxes, regulatory barriers, or a lack of competing operators often lead to limited downward pressure on prices. In many cases, the absence of competitive infrastructure investment keeps data expensive and slow.

Why Headline Prices Vary From Real-World Experience

These figures typically represent standardized USD-per-GB calculations. They do not always reflect discounted bundles, special promotions, or varying daily usage packages. However, even within bundle structures, affordability remains limited relative to average incomes, meaning the digital divide persists even when the “official” price seems lower.

The Turning Point: How LEO Satellites Will Reshape Connectivity

While terrestrial networks have long defined Africa’s connectivity landscape, Low-Earth Orbit (LEO) satellite technology is now emerging as the most significant disruptor in decades.

1. Independent of Terrain and Distance

LEO satellites bypass mountains, oceans, sparse populations, and unreliable grids. They deliver high-speed connectivity to locations where fiber and mobile networks are difficult—or economically impossible—to deploy.

2. Consistently Low Latency & High Capacity

Unlike traditional geostationary satellites, LEO systems operate much closer to Earth, enabling performance comparable to terrestrial broadband. This means video streaming, remote work, real-time calls, cloud access, and online learning become viable in zones previously denied such capabilities.

3. Competitive Pressure on Traditional Operators

As LEO providers enter the market with reliable, high-speed connections, incumbent mobile operators face new incentives to reduce prices, improve service quality, and modernize infrastructure.

4. Expanding Universal Access

For rural, coastal, island, and sparsely populated regions—places currently appearing on the “most expensive data” rankings—LEO satellites offer the first realistic path toward affordable, stable, and high-capacity internet access.

For companies like AfrikaStar, the mission is clear:

bring modern LEO-powered connectivity to homes, schools, and businesses across the continent, ensuring that price and geography no longer determine who can participate in the digital world.

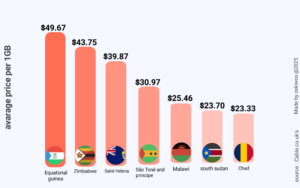

Across Africa, the cost of mobile data remains one of the strongest indicators of digital inequality. According to the comparative dataset you provided (Cable.co.uk), several markets stand out for exceptionally high prices. At the top of the list is Equatorial Guinea (~$49.67/GB), followed by Zimbabwe (~$43.75/GB), Saint Helena (~$39.87/GB), and São Tomé and Príncipe, placing fourth.

Across Africa, the cost of mobile data remains one of the strongest indicators of digital inequality. According to the comparative dataset you provided (Cable.co.uk), several markets stand out for exceptionally high prices. At the top of the list is Equatorial Guinea (~$49.67/GB), followed by Zimbabwe (~$43.75/GB), Saint Helena (~$39.87/GB), and São Tomé and Príncipe, placing fourth.